Olddog wrote:Maybe that when your cancellation numbers are mostly conversion orders registered that way ?

Good point. Cancellations can also be conversions. It is why we have to be careful just looking at gross orders numbers.

Moderators: richierich, ua900, PanAm_DC10, hOMSaR

Olddog wrote:Maybe that when your cancellation numbers are mostly conversion orders registered that way ?

benbeny wrote:How in the world they're able to find enough pax (and airports) for that amount of new planes every month? Even with ultra-rapid growth of LCC in Asia and other places, I don't see enough pax to fill them up. The market will soak up eventually, and the growth will slow down. And let's not talk about airport congestion everywhere.

Now, we can talk about the real bubble here.

unrave wrote:Newbiepilot wrote:

What i see as a problem is how big some of the orders are from relatively small airlines. IndiGo, Air Asia, Lion Air, and Indigo Partners ordered for massive expansion that exceeds market growth rates. That means either those orders wont be fully taken up, may get deferred, or some other airline will be out out of business or shrink (like Monarch or Air Berlin). That could create a bubble of used planes

This reads awfully similar to the hordes of sceptic comments made by Anetters 13 years back when IndiGo placed its first 100 aircraft order. Not only did it take delivery of all of them, it now operates more than 150. Unless some dramatic economic downturn I don't see why an airline that controls 40% of the fastest growing aviation market that is projected to become grow 4x in 20 years wouldn't be able to operate a fleet of 300 aircraft (accounting for replacements). All the jumbo airlines of the world today - Southwest, Ryaniar, Easyjet - would have gone through a similar phase of hectic growth.

RalXWB wrote:Sad to see another Anet-myth is still alive. "Most A320 orders are from unstable airlines or won´t be fully taken up or will be deferred or will be cancelled or orderbook inflation or order bubble or whatever". If there is a bubble or something similar it affects all types and not just one type of one producer...smh. If Airbus increases the production rate, they do it for a reason.

Newbiepilot wrote:It isn’t most orders will be cancelled, deferred, etc. The reality is that Airbus has had a 17% cancellation rate over the past three years when looking at net in year of cancellation. (I averaged three years since last year’s 23% cancellation rate was a bit of an anomaly and some may want to look at numbers differently). This factors in some conversions. The myth is that sales numbers don’t lie. With longer and longer backlogs and bigger and bigger orders stretching longer, there is a level of order inflation going on,

WIederling wrote:Newbiepilot wrote:It isn’t most orders will be cancelled, deferred, etc. The reality is that Airbus has had a 17% cancellation rate over the past three years when looking at net in year of cancellation. (I averaged three years since last year’s 23% cancellation rate was a bit of an anomaly and some may want to look at numbers differently). This factors in some conversions. The myth is that sales numbers don’t lie. With longer and longer backlogs and bigger and bigger orders stretching longer, there is a level of order inflation going on,

Absolute numbers don't tell much. How do you assay order changes to different subtypes or to a completely different type.

I'd compare volatility of orders between the big airframers.

( We do have this statement about "Boeing has the "better" customers in their orderbook sitting in the corner.)

Newbiepilot wrote:With all due respect this thread is about Airbus potentially increasing their production rate and some concerns lessors have regarding a bubble. It is not an A vs B, who has the better backlog thread. If Airbus goes up to 70 planes a month and there is a Southeast Asia financial crisis, India has a recession, SARS outbreak, Us stock market collapse, etc there is risk that the rate will be too high and there could be a glut of used planes on the market.

Newbiepilot wrote:It isn’t most orders will be cancelled, deferred, etc. The reality is that Airbus has had a 17% cancellation rate over the past three years when looking at net in year of cancellation. (I averaged three years since last year’s 23% cancellation rate was a bit of an anomaly and some may want to look at numbers differently). This factors in some conversions. The myth is that sales numbers don’t lie. With longer and longer backlogs and bigger and bigger orders stretching longer, there is a level of order inflation going on,

astuteman wrote:Newbiepilot wrote:It isn’t most orders will be cancelled, deferred, etc. The reality is that Airbus has had a 17% cancellation rate over the past three years when looking at net in year of cancellation. (I averaged three years since last year’s 23% cancellation rate was a bit of an anomaly and some may want to look at numbers differently). This factors in some conversions. The myth is that sales numbers don’t lie. With longer and longer backlogs and bigger and bigger orders stretching longer, there is a level of order inflation going on,

In the last 3 years Boeing have experienced an 18.5% "cancellation" rate net in the year of cancellation over the last 3 years.

So what are you trying to say?

Are you really trying to suggest that Airbus sit on a 6 200 x A320 backlog and Boeing on a 4 600 x 737 backlog after 17% and 18.5% net "cancellations" respectively? If anything that would indicate the backlogs are even more robust than they look.

These are virtually ALL conversions, for both A and B.

Cancellation can, and do lie.

Airbus have NOT had 17% of net orders cancelled

Ever since I joined this website, Airbus have been criticised for having a more aggressive approach to market share by either

a) taking greater risks than Boeing, or

b) selling at cost or below

I would challenge you to come up with a meaningful statistic that shows that cancellations i.e. NOT conversions, have had a meaningfully different impact on either manufacturer over the last 15 years.

Airbus have a greater proportion of order in the faster growing economies. That is a fact. It is also a fact that this was the case during the GFC in 2008 and 2009.

And yet both production rates and backlogs held up in that period.

From the selling price viewpoint, last year's Airbus results, especially the Q4 ones when some of the inventory got delivered, clearly demonstrate that Airbus are making double digit margin on the A320's they are selling.

So Airbus are not engaging in either speculative orders or dumping just to make up numbers.

This is a bus that A-net needs to disembark from

I get a feeling that some people think that Airbus is run by A-net teenagers.

It isn't.

All of these orders go through strict LCM governance.

And historically it has shown to be robust.

It has been the case over the last 15 years that the 20 year forecast for narrobodys from both manufacturers has consistently gone up, year-on-year

Airbus last year forecast 25 000 narrowbodys over 20 years. In 2010 this number was 17 800

Boeing last year forecast 29 500 narrowbodys over 20 years. In 2010 this number was 21 000.

What are these numbers going to be in c. 2022 which is the earliest that rates like this are likely to be achieved.

The current "order inflation" rate in the OEM's market forecasts is 1000 per year.

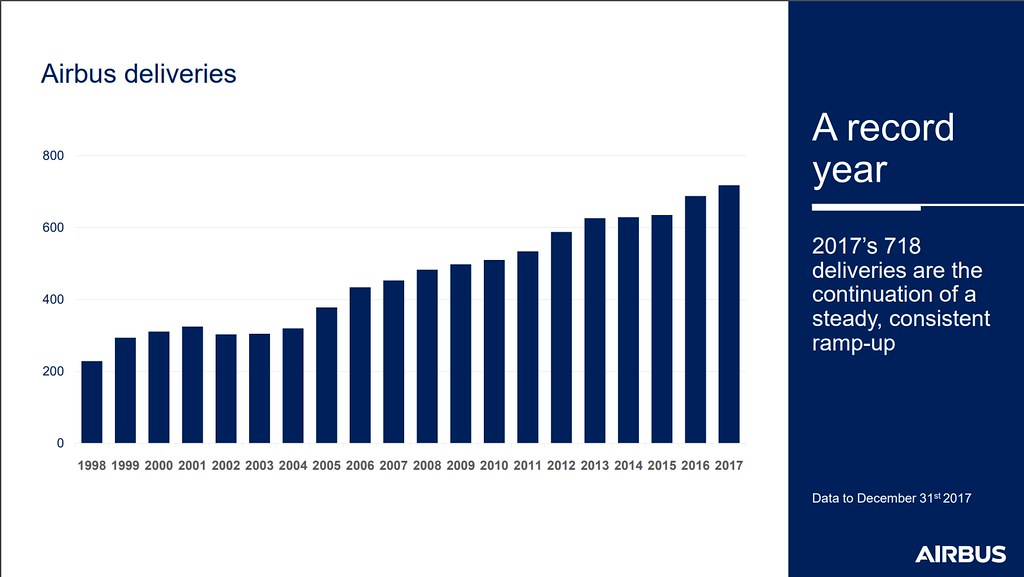

Last year Boeing delivered 530 narrowbodys and Airbus delivered (by some miracle or other) delivered 550

That's on target for 21 600 deliveries in 20 years.

It just isn't enough

As an aside, the big two will want to keep the market as saturated as possible to deter new entrants.

If they go up to, say 800 and 700 respectively for A and B by 2022, but have to throttle back briefly to 700 and 600 for a couple of years, is that really a bubble?

Rgds

astuteman wrote:I get a feeling that some people think that Airbus is run by A-net teenagers.

astuteman wrote:Newbiepilot wrote:It isn’t most orders will be cancelled, deferred, etc. The reality is that Airbus has had a 17% cancellation rate over the past three years when looking at net in year of cancellation. (I averaged three years since last year’s 23% cancellation rate was a bit of an anomaly and some may want to look at numbers differently). This factors in some conversions. The myth is that sales numbers don’t lie. With longer and longer backlogs and bigger and bigger orders stretching longer, there is a level of order inflation going on,

In the last 3 years Boeing have experienced an 18.5% "cancellation" rate net in the year of cancellation over the last 3 years.

So what are you trying to say?

Are you really trying to suggest that Airbus sit on a 6 200 x A320 backlog and Boeing on a 4 600 x 737 backlog after 17% and 18.5% net "cancellations" respectively? If anything that would indicate the backlogs are even more robust than they look.

These are virtually ALL conversions, for both A and B.

Cancellation can, and do lie.

Airbus have NOT had 17% of net orders cancelled

Ever since I joined this website, Airbus have been criticised for having a more aggressive approach to market share by either

a) taking greater risks than Boeing, or

b) selling at cost or below

I would challenge you to come up with a meaningful statistic that shows that cancellations i.e. NOT conversions, have had a meaningfully different impact on either manufacturer over the last 15 years.

Airbus have a greater proportion of order in the faster growing economies. That is a fact. It is also a fact that this was the case during the GFC in 2008 and 2009.

And yet both production rates and backlogs held up in that period.

From the selling price viewpoint, last year's Airbus results, especially the Q4 ones when some of the inventory got delivered, clearly demonstrate that Airbus are making double digit margin on the A320's they are selling.

So Airbus are not engaging in either speculative orders or dumping just to make up numbers.

This is a bus that A-net needs to disembark from

I get a feeling that some people think that Airbus is run by A-net teenagers.

It isn't.

All of these orders go through strict LCM governance.

And historically it has shown to be robust.

It has been the case over the last 15 years that the 20 year forecast for narrobodys from both manufacturers has consistently gone up, year-on-year

Airbus last year forecast 25 000 narrowbodys over 20 years. In 2010 this number was 17 800

Boeing last year forecast 29 500 narrowbodys over 20 years. In 2010 this number was 21 000.

What are these numbers going to be in c. 2022 which is the earliest that rates like this are likely to be achieved.

The current "order inflation" rate in the OEM's market forecasts is 1000 per year.

Last year Boeing delivered 530 narrowbodys and Airbus delivered (by some miracle or other) delivered 550

That's on target for 21 600 deliveries in 20 years.

It just isn't enough

As an aside, the big two will want to keep the market as saturated as possible to deter new entrants.

If they go up to, say 800 and 700 respectively for A and B by 2022, but have to throttle back briefly to 700 and 600 for a couple of years, is that really a bubble?

Rgds

Newbiepilot wrote:Ok then, so given all that you said, do you think 70 airplanes a month is a reasonable production rate? I intentionally tried to avoid an A vs B discussion, but they have issues too with their production rate and competition if there is a downturn.astuteman wrote:I get a feeling that some people think that Airbus is run by A-net teenagers.

Do you really view my post as thinking that? Ouch. My post was in response to RALXWB’s post about a myth that I don’t believe exists.

I am surprised you don’t see the order inflation going on. I understand your points and I have seen some of those exaggerated criticisms of Airbus before, but that doesn’t mean they are all entirely untrue. Do you really think that all the orders from airlines like Frontier, IndiGo, GoAir, Jetsmart, Volaris, Vietjet, Air Asia, Lion Air, etc don’t represent inflation and the potential for a bubble? For all those planes to be delivered, there will likely be some other airlines contracting or going out of business, which could lead to cheaper used aircraft on the market.

astuteman wrote:Newbiepilot wrote:It isn’t most orders will be cancelled, deferred, etc. The reality is that Airbus has had a 17% cancellation rate over the past three years when looking at net in year of cancellation. (I averaged three years since last year’s 23% cancellation rate was a bit of an anomaly and some may want to look at numbers differently). This factors in some conversions. The myth is that sales numbers don’t lie. With longer and longer backlogs and bigger and bigger orders stretching longer, there is a level of order inflation going on,

In the last 3 years Boeing have experienced an 18.5% "cancellation" rate net in the year of cancellation over the last 3 years.

So what are you trying to say?

Are you really trying to suggest that Airbus sit on a 6 200 x A320 backlog and Boeing on a 4 600 x 737 backlog after 17% and 18.5% net "cancellations" respectively? If anything that would indicate the backlogs are even more robust than they look.

These are virtually ALL conversions, for both A and B.

Cancellation can, and do lie.

Airbus have NOT had 17% of net orders cancelled

Ever since I joined this website, Airbus have been criticised for having a more aggressive approach to market share by either

a) taking greater risks than Boeing, or

b) selling at cost or below

I would challenge you to come up with a meaningful statistic that shows that cancellations i.e. NOT conversions, have had a meaningfully different impact on either manufacturer over the last 15 years.

Airbus have a greater proportion of order in the faster growing economies. That is a fact. It is also a fact that this was the case during the GFC in 2008 and 2009.

And yet both production rates and backlogs held up in that period.

From the selling price viewpoint, last year's Airbus results, especially the Q4 ones when some of the inventory got delivered, clearly demonstrate that Airbus are making double digit margin on the A320's they are selling.

So Airbus are not engaging in either speculative orders or dumping just to make up numbers.

This is a bus that A-net needs to disembark from

I get a feeling that some people think that Airbus is run by A-net teenagers.

It isn't.

All of these orders go through strict LCM governance.

And historically it has shown to be robust.

It has been the case over the last 15 years that the 20 year forecast for narrobodys from both manufacturers has consistently gone up, year-on-year

Airbus last year forecast 25 000 narrowbodys over 20 years. In 2010 this number was 17 800

Boeing last year forecast 29 500 narrowbodys over 20 years. In 2010 this number was 21 000.

What are these numbers going to be in c. 2022 which is the earliest that rates like this are likely to be achieved.

The current "order inflation" rate in the OEM's market forecasts is 1000 per year.

Last year Boeing delivered 530 narrowbodys and Airbus delivered (by some miracle or other) delivered 550

That's on target for 21 600 deliveries in 20 years.

It just isn't enough

As an aside, the big two will want to keep the market as saturated as possible to deter new entrants.

If they go up to, say 800 and 700 respectively for A and B by 2022, but have to throttle back briefly to 700 and 600 for a couple of years, is that really a bubble?

Rgds

Olddog wrote:If you are nervous with that rate, try to imagine that rate + 10 - 15 CS 100/Cs 300 each month

william wrote:But I understand Airbus's moves on this, its to monetize the backlog, why wait 7 years when you can get paid in 5.

william wrote:I wonder what all of these NBs A and B does to the lease market.

Newbiepilot wrote:Ok then, so given all that you said, do you think 70 airplanes a month is a reasonable production rate? I intentionally tried to avoid an A vs B discussion, but they have issues too with their production rate and competition if there is a downturn.

I am surprised you don’t see the order inflation going on. I understand your points and I have seen some of those exaggerated criticisms of Airbus before, but that doesn’t mean they are all entirely untrue. Do you really think that all the orders from airlines like Frontier, IndiGo, GoAir, Jetsmart, Volaris, Vietjet, Air Asia, Lion Air, etc don’t represent inflation and the potential for a bubble? For all those planes to be delivered, there will likely be some other airlines contracting or going out of business, which could lead to cheaper used aircraft on the market.

Bricktop wrote:Maybe I am dense, but when these orders (WB or NB, Airbus or Boeing), don't they have a delivery period listed? Then it should be simple enough (even stupid me can put together an Excel spreadsheet) to know what the rate should be. I have to deliver so many in each year contractually, right? Simple math, or simple Bricktop? Discuss.

scbriml wrote:Given the backlog and order rate, I’d say 70/month is a necessity.

...

I don’t see “order inflation”. If you put any store by both OEMs market forecasts, then order rate is pretty close (if anything slightly low). Deliveries need to catch up.

QuarkFly wrote:scbriml wrote:Given the backlog and order rate, I’d say 70/month is a necessity.

...

I don’t see “order inflation”. If you put any store by both OEMs market forecasts, then order rate is pretty close (if anything slightly low). Deliveries need to catch up.

Hmmm, So Airbus A320 goes to 70 a month, Boeing 737 is already going to 57 a month next year (rumors of 60 or more?), plus C-Series...Sure Asia, Middle-East and Africa are growing...but this translates into close to 150 narrow-bodies a month or 1700-1800 a year and eventually more after 2020. At that rate, the market will have to absorb about 20,000 narrow-bodies in a decade -- that is close to the 20 year forecasts, not ten year...Something is not right here!

And we are now heading into a higher interest rate environment, oil prices are reasonable due to fracking, so no great need to dump older frames...Some talk of 10 to 12 year old A320 and 737NG being scrapped? -- that has to be very rare.

Yes, I'll stick my neck out and call it a bubble !!

QuarkFly wrote:scbriml wrote:Given the backlog and order rate, I’d say 70/month is a necessity.

I don’t see “order inflation”. If you put any store by both OEMs market forecasts, then order rate is pretty close (if anything slightly low). Deliveries need to catch up.

Hmmm, So Airbus A320 goes to 70 a month, Boeing 737 is already going to 57 a month next year (rumors of 60 or more?), plus C-Series...Sure Asia, Middle-East and Africa are growing...but this translates into close to 150 narrow-bodies a month or 1700-1800 a year and eventually more after 2020. At that rate, the market will have to absorb about 20,000 narrow-bodies in a decade -- that is close to the 20 year forecasts, not ten year...Something is not right here!

And we are now heading into a higher interest rate environment, oil prices are reasonable due to fracking, so no great need to dump older frames...Some talk of 10 to 12 year old A320 and 737NG being scrapped? -- that has to be very rare.

Yes, I'll stick my neck out and call it a bubble !!

LA704 wrote:

Thing is they were ordered with low oil prices though. So they were more economical than old planes with cheap fuel, despite ownership or capital cost. If oil prices rise, the demand for MAX and neo will rise accordingly, just to save the cash flow (sacrificing CAPEX). The freight markets recover and the first NGs/CEOs are in conversion. The markets get even more fragmented, so in the end I imagine the widebodies suffer more than any narrowbody. .

zeke wrote:This is exactly what the economists are predicting, eg http://avolon.aero/wp/wp-content/upload ... F_2014.pdf

astuteman wrote:Newbiepilot wrote:Ok then, so given all that you said, do you think 70 airplanes a month is a reasonable production rate? I intentionally tried to avoid an A vs B discussion, but they have issues too with their production rate and competition if there is a downturn.astuteman wrote:I get a feeling that some people think that Airbus is run by A-net teenagers.

Do you really view my post as thinking that? Ouch. My post was in response to RALXWB’s post about a myth that I don’t believe exists.

I am surprised you don’t see the order inflation going on. I understand your points and I have seen some of those exaggerated criticisms of Airbus before, but that doesn’t mean they are all entirely untrue. Do you really think that all the orders from airlines like Frontier, IndiGo, GoAir, Jetsmart, Volaris, Vietjet, Air Asia, Lion Air, etc don’t represent inflation and the potential for a bubble? For all those planes to be delivered, there will likely be some other airlines contracting or going out of business, which could lead to cheaper used aircraft on the market.

I think I answered your first question.

Yes, I think 70 per month is reasonable, even with a bit of "froth" in the market.

It's clear it will take 3-4 years to get there.

And even then at say 800 per year (c 11.5 months per year output) it still represents a backlog of 7 1/2 years production.

That is still too long. I think genuine cancellations will be small. There may be more deferrals

There has never been backlogs this long measured in years of production.

Even if the backlog shrank to say 4 800, which it won't, that would still represent 6 years at 800 a year, plenty of time to adjust if needed

.

I don't see anything materially different to the trend of the last decade. Which for me is a story of strong growth in fragmentation driven by narrobodys.

As a Boeing fan (not "fanboy" I hasten to add) I would have expected you to buy into your company's belief in fragmentation a bit more.

They are clearly right.

That's the "inflation" that I see.

It's not a bubble.

As for the A-net teenager thing - apologies - it was a general statement, and not aimed at your comments

Is there risk in the backlogs?

Yes. There will be downturns, cancellations, and deferrals.

But there have always been these.

I don't think today is any different

Rgds

mjoelnir wrote:The situation is really very simple, you have customers that order merchandise and you run a production to fulfill those orders. It makes more sense for Airbus to go to 70 frames a month on the A320 family, than it is for Boeing to go to 14 a month on the 787 family.

zeke wrote:Couldn’t agree more, I think it also makes more sense to have the FAL production expansion outside of Europe.

The new FALs I think are easier to expand.

william wrote:I wander what all of these NBs A and B does to the lease market. After Indigo finishes using its A320s for five or six years who is buying that aircraft from the lessor? There are only so many Allegiants, Deltas and Uniteds in the world snapping up used aircraft.

http://www.business-standard.com/articl ... 085_1.html

The reason this conversation is related to this thread is that about half of A and B NB backlog will be sale leasebacks, and eventually the returns start competing with the new product. Do not know when we get to that point but it can't be far off.

But I understand Airbus's moves on this, its to monetize the backlog, why wait 7 years when you can get paid in 5.

Oh well, I guess the ME3 will have to do the job.

Oh well, I guess the ME3 will have to do the job.Newbiepilot wrote:Olddog wrote:If you are nervous with that rate, try to imagine that rate + 10 - 15 CS 100/Cs 300 each month

I wonder about that too

mjoelnir wrote:The situation is really very simple, you have customers that order merchandise and you run a production to fulfill those orders. It makes more sense for Airbus to go to 70 frames a month on the A320 family, than it is for Boeing to go to 14 a month on the 787 family.

zeke wrote:Couldn’t agree more, I think it also makes more sense to have the FAL production expansion outside of Europe.

The new FALs I think are easier to expand.

Newbiepilot wrote:mjoelnir wrote:The situation is really very simple, you have customers that order merchandise and you run a production to fulfill those orders. It makes more sense for Airbus to go to 70 frames a month on the A320 family, than it is for Boeing to go to 14 a month on the 787 family.

From a pure numbers point I won’t dispute how simple it sounds. The problem is the two years it takes to adjust production rates and whether or not the supply chain can support it. It is rather apparent the engine production lines are a problem. There likely are other challenging areas too that aren’t getting the media attention. Galleys, lavatories, and seats were a big problem on the A350 recently. Those components don’t sound the most complicated, but they can stop deliveries.

The production challenge is one side making it harder to ramp up production and then risk white tails and overproduction due to economic factors is on the other side if production is too high. Determine ideal production rate is far from simple.

Is 70 the best rate? Time will tell if Airbus decides to do so. I believe they are studying it from the original information posted in this thread.

flee wrote:

So, why are people still talking about order bubbles?

Newbiepilot wrote:flee wrote:

So, why are people still talking about order bubbles?

Some of us remember 2003 and/or 2009. Many in the industry were laid off due to cycles and remember them. Going down in rate and the consequences of it can be very painful. I am not saying 70 per month is sustainable, and I agree bubble may be the wrong word, but these huge order backlogs do represent a shift in the industry

Newbiepilot wrote:flee wrote:

So, why are people still talking about order bubbles?

Some of us remember 2003 and/or 2009. Many in the industry were laid off due to cycles and remember them. Going down in rate and the consequences of it can be very painful. I am not saying 70 per month is sustainable, and I agree bubble may be the wrong word, but these huge order backlogs do represent a shift in the industry

Newbiepilot wrote:Overbooking might be the solution to get them through an economic downturn.

Newbiepilot wrote:Some of us remember 2003 and/or 2009. Many in the industry were laid off due to cycles and remember them. Going down in rate and the consequences of it can be very painful. I am not saying 70 per month is sustainable, and I agree bubble may be the wrong word, but these huge order backlogs do represent a shift in the industry

lightsaber wrote:Oh, I just looked at Boeing's CMO, 41,030 or over 2,000 aircraft per year! When will we see that production rate?

http://www.boeing.com/commercial/market ... look-2017/

Airbus is predicting only 35,000 new aircraft:

http://www.airbus.com/aircraft/market/g ... Lightsaber

zeke wrote:This is exactly what the economists are predicting, eg http://avolon.aero/wp/wp-content/upload ... F_2014.pdf

QuarkFly wrote:lightsaber wrote:Oh, I just looked at Boeing's CMO, 41,030 or over 2,000 aircraft per year! When will we see that production rate?

http://www.boeing.com/commercial/market ... look-2017/

Airbus is predicting only 35,000 new aircraft:

http://www.airbus.com/aircraft/market/g ... Lightsaberzeke wrote:This is exactly what the economists are predicting, eg http://avolon.aero/wp/wp-content/upload ... F_2014.pdf

A lot of happy talk on this thread -- like pre-financial bubble..."It goes on forever !!" ...

Single-isle forecasts over the next 20-years...Airbus:24807, Boeing: 29530, Avalon: 25300 ...But each of these forecasts include 100-seat aircraft too...such as as E190/95,, CRJ-100 and CS100 -- Also it is possible C919 could take a decent chunk of the China market over the next 20 years So drop the A320 -737 forecasts to less than 25K frames, maybe a lot less (I love C-series)

1250 aircraft a year is 25K frames in twenty years...we are above that production rate now at the beginning of the 20 year time-frame !! That's what's wrong here! Some 20-year possibilities...

- High interest rates make financing much more difficult,

- Alternative energy and high-speed rail (China) drop fuel prices so that well maintained A320 / 737NG stay in fleets for 25-30 years.

- NMA and/or A321X 250-passenger aircraft siphon off demand from A320 / 738 ...e.g. LCC routes become 2-3 times per day with 250 passengers instead of 4-5 times per day with 150 passengers...Freeing up aircraft and reducing deliveries.

- North Korea, Middle-East is a mess...

- MAGA and Brexit politicians screw up the world economy, etc.

And it is possible for forecasts to be too high (A380, 747-8). There has not been a "Turn Out the Lights" downturn in Seattle or Toulouse for decades...it can happen. Nobody ever predicts it ahead of time, and aircraft down-cycles can be ugly.

lightsaber wrote:Please point me to one Airbus or Boeing study that over predicted demand. All I've seen significantly underpredicted demand.

lightsaber wrote:High interest rates only come if countries like China are willing to let their currency rise with the associated plunge in exports. I expect higher rates, but only approaching the historical 7%. The Euro is done if it goes higher.

I assume 64 to be possible without building a new FAL, TSN and BFM could move to 8 a month.

That's right, XFW recently got a 4th FAL, built in former A380 facilities after the A380 ramp-down. However, A320 cabin outfitting for the TLS built aircraft was moved to TLS.The last FAL expansion for the A320 family happened in XFW .